This post is brought to you by Credit Sesame. All opinions are my own.

Establishing credit can be difficult at first, but, once you get past that, you should be free sailing your way to a great credit score! Actually, there’s much more to it than that. It takes a lot of good money habits to reach and maintain a great credit score. I’d like to share with you how I established credit for myself and now how I plan to improve my current score so I can pay less for the money I want to borrow.

I was fresh out of high school, working two jobs, living with my sister and brother-in-law, and I had no credit to my name.

My parents never got me a credit card with my name on it.

I bought my first car with a loan from my dad.

I got on a cell phone plan with my sister and her husband.

I was an “adult,” but I still had to rely on others to make it in this world.

It wasn’t until my brother-in-law brought up the topic at dinner one night that I even started thinking about establishing credit. He told me that one of the best ways to start building my credit was to buy something from our local home furnishings store with that store’s credit card. So I went there and qualified to purchase a car stereo. I paid it off within a couple of months. Was building credit really that easy?

Alas, there is a lot more to establishing credit than just applying for a store credit card and paying the minimum each month. It has taken many years of many different purchases to really establish my own credit. Since that first financed car stereo I have opened a credit card account, taken out student loans, purchased a car, and bought a house.

© Fantasista / Dollar Photo Club

© Fantasista / Dollar Photo Club

As I worked my way up from the smaller loans to the biggest ones, my credit score became more and more important. Had I gone to a mortgage lender with a credit score of 630 to my name, my interest rate would have been through the roof. Fortunately when I applied to buy a house with my husband my credit score was a lot higher than 630. Not perfect, but pretty good. Unfortunately, since I was not working when we applied, they used my husband’s credit score which was not quite as impressive as mine.

Because of this fact, we are paying a higher-than-normal mortgage insurance premium. Honestly, we should have waited until we had at least 20% to put down before even thinking of buying a house, but that’s a post for another day.

If we would have had a way to monitor our credit scores during that home-buying period we would have been able to increase my husband’s score before buying a house and locking in a high mortgage insurance premium. If his score had been a little higher, we would have saved at least $100 each month on our mortgage!! We have spent $2,400 more since we started paying for our house two years ago because of this little misstep.

To make things very clear, you need to improve your credit score if you want to borrow money for anything (unless your score is excellent of course).

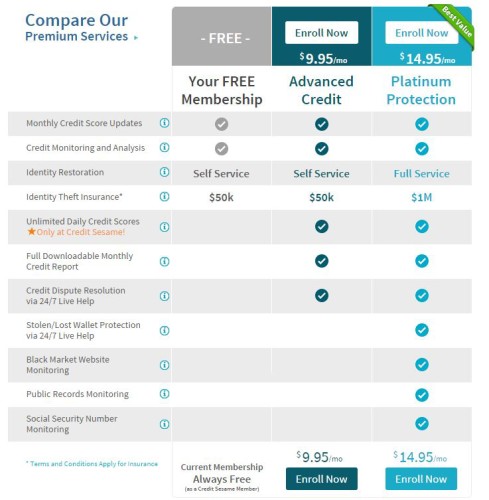

Credit Sesame – A Free Way to Check Your Score

Before you can improve your credit score, you have to know what your score is. You can easily check that for free, on a monthly basis, with Credit Sesame.

Credit Sesame is a website that shows you your credit score, monitors and analyzes your credit, and protects you against identity theft up to $50k. This is all completely free, mind you! There is no catch, and you never have to give them your credit card number. Of course, they also have a paid version, but most people will probably find the free version exactly what they need.

Drawbacks to using just the free version:

- You will not receive a free credit report. All they show you is the score, but they show you all the things that are affecting that score which are just as important.

- You can only get $50 thousand in identity theft protection. But, seriously, that’s a whole lot of money for just having a free account.

- It may not be as accurate as the paid versions. My own account states that our home’s value is 3.5 times more than it really is. The interest rate that it shows for that home loan is also way off. So you obviously get what you pay for in this instance.

How Can Credit Sesame Help You Achieve a Better Credit Score?

If you’re looking to improve your credit score, here is how using a free account on Credit Sesame can help you:

Payment History

Your account will show you all the late payments you have made over a certain time period, as well as collections, foreclosures, and bankruptcies. If you know you have a couple late payments on your report, you can at least start anew and resolve to do better. It might not help your credit score for quite awhile, but you’ll be glad you worked hard once it does.

Credit Utilization

Under your account you can see how much of your credit you are actually using. The ideal level is 10% or less. Mine is showing a level of 18%. If you are using more than 10%, you can try to lower your balances.

Say you have two credit cards and between them the most amount you can borrow each month is $3,000. On one card you have a balance of $800 and on the other one you owe $320. Your total balance is $1,120 out of $3,000. That means you are using 37% of your credit limit. Now you know that if you want to improve your credit score, you need lower balances on both cards. Do your best to pay as much as you can towards each one each month. In time, your balances will become lower and your credit score will improve.

Credit Inquiries

Credit Inquiries

Your Credit Sesame account will show you how many times you have applied for credit in the last year. This is useful if you happen to be applying too much, which negatively affects your score. If you are going to switch cell phone carriers, for example, you should wait a few months so you don’t add another inquiry to your credit history.

Credit Overextension

Under “Debt Analysis” on your Credit Sesame account, it shows you how much of your monthly income goes toward paying for your credit (that is, if you input an accurate salary). While this percentage won’t hurt your credit score, it will become a problem if you can’t pay for the credit you are using. Before you buy a house, you should get this number as low as possible or you might not qualify for a loan. Knowing that you are overextended can make you think twice about trying to apply for another loan.

Account Mix

Having a variety of accounts (i.e. credit cards, home loans, auto loans, and student loans) is beneficial to your credit score. Your account will show you how many different accounts you have on your credit history. It will give you a rating on whether this is excellent, ok, or poor. If you are in the poor zone, this might mean you need more accounts. Maybe you have 3 credit cards and nothing else. Consider getting rid of one or two credit cards and getting an auto loan instead. Don’t go crazy though, because you don’t want the other areas we have already discussed to be affected.

Age of Credit History

You should be able to see how long your credit history is. Mine shows a length of 10 years and 8 months. My average length of all accounts is 5 years and 7 months. Creditors want to see that you have established credit for at least 5 years. The only thing you can do if your credit history is only a couple years old is to keep paying on the loans you have.

I used to think that you should close unused accounts, but even if you’re no longer using a credit card or loan, it can improve your credit score if you’ve had it for quite some time.

In short, here’s a quick list of ways to increase your credit score:

- Pay on time, every time

- Use 10% or less of the credit that you have qualified for

- Only apply for credit when you actually need it

- Apply for credit that you can actually afford

- Have a variety of accounts: credit cards, auto loans, student loans, mortgage

- Just keep up with your good habits over time

If you desire to spend less on the money you borrow, it is essential that you know how to improve your credit score, and what better way than with a free account with Credit Sesame. I’d say it’s a no brainer!

- Versatile and Flavorful Pumpkin Chicken Soup - 01.03.26

- Easy Instant Pot Bone Broth Recipe - 09.20.25

- Healthy Make-Ahead Tomato Onion Salad Jars - 07.11.25

You’re right about credit not being established overnight. It does take awhile and multiple purchases to build a positive history.

There are many people who are not aware of how important it is to maintain a good credit score until a situation comes whereby a bad credit score creates an issue in getting a mortgage or so. Everyone has their own financial situations which vary person to person based on their salary, other income sources, bank balance etc. The story you shared is really going to help many other home buyers’ especially first time home buyers. Everyone should keep a good credit card score to get maximum benefits. This is one of the important tips I share with my clients who look for mortgages for home buying.